Singapore’s public housing model has been lauded as one of the best in the world. It has been well designed and worked well for many Singaporeans for decades. Thus, when HDB announced a new Prime Location Housing (PLH) model, you know it’s a big deal and you better tune in to it.

Here’s what you need to know about the HDB PLH model in just 8 minutes.

What is the HDB PLH Model?

Announced on 27th October 2021, the HDB PLH model is a new mechanism introduced to rein in the “lottery effect”.

For those unfamiliar with the term “lottery effect”, it refers to how lucky homebuyers who managed to snap up homes in prime locations when balloting for a HDB BTO could enjoy a profiting phenomenon when flipping their property.

The chances of securing one of these units are completely up to chance, hence "lottery effect". The most prominent example is Pinnacle@Duxton, where many units have been sold for $1 million or more.

Who Is Eligible To Purchase in the HDB PLH Model?

Under the HDB PLH model, homebuyers for BTOs in what HDB has referred to as prime, central locations will be subjected the same eligibility requirements for HDB BTOs.

However, there are new restrictions for purchase of PLH resale flats. Unlike typical resale flats, PLH resale flats can only be sold to buyers who are eligible for HDB BTOs.

That means, in order to purchase HDB flats under the PLH model, you need to be married or have the intention to get married, i.e. under the Fiancé/Fiancée Scheme. As there are currently no 2-room Flexi flats in the PLH model, this means that singles will not be eligible to apply for PLH flats in the BTO exercise, nor buy them on the resale market.

Apart from your marital status, you and your partner also need to be under the prevailing income ceiling, which currently is $14,000. This applies not only when you apply for the BTO, but also for resale flats under the PLH model.

Besides that, neither you nor your partner can own a private property in the last 30 months. One of you also needs to be a Singaporean in order to apply.

Which Area Does the HDB PLH Model Affect?

While there is no clear mention of what constitutes prime, central locations under the HDB PLH model, we can find clues from various sources.

Source: URA

For instance, URA Master Plan has a clearly defined region for the Central Area (not to be confused with the surrounding Central Region). Under URA Master Plan 2019, Central area includes Rochor, Bugis, the Central Business District (CBD), Marina Bay, and Orchard. The first BTO under HDB PLH model is in Rochor, which confirms this hypothesis.

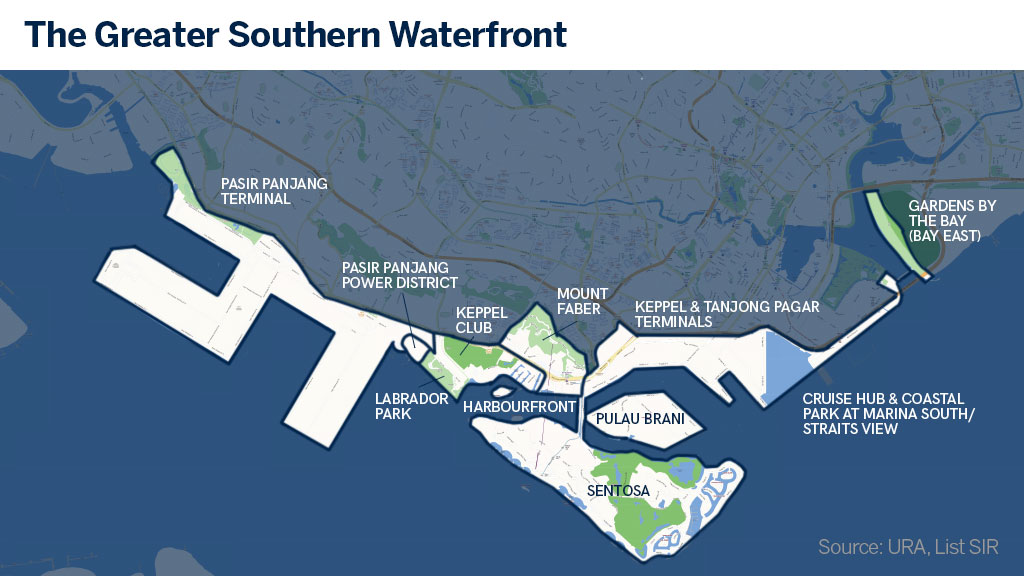

Source: List International Realty

Besides the area around CBD and Orchard, another area that will most likely fall under the Central area classification is the Greater Southern Waterfront (GSW). The moment GSW was mentioned in the 2019 National Day Rally, commentary about affordability of public housing in such prime areas became hot topics.

Given the potentially high price point of properties in GSW, it will likely require higher subsidy to keep the area affordable. The higher subsidy will only apply if the area falls under Central area classification.

What Kind Of "Privileges" Do You Need To Forgo If You Want To Qualify For HDB PLH Model?

Compared to ordinary HDB BTOs, BTOs under the HDB PLH model comes with additional restrictions.

1. 10-Year MOP vs 5-Year MOP

The most poignant restriction is the 10-year Minimum Occupation Period (MOP). Usual BTOs only come with a 5-year MOP. But for those under the PLH model, it comes with a 10-year MOP. If you are thinking about upgrading to condo, the long MOP might put you off.

2. No Rental Of Whole Unit Even After MOP

Besides doubling the MOP to 10 years, the HDB PLH model also disallow homeowners to rent out the whole unit after the MOP. You can only rent out “spare rooms” in the home. This is unlike ordinary BTOs where you can rent out the whole unit after the MOP.

With this restriction, there’s little upside for those who wants to own multiple properties (e.g. buying a condo after MOP reaches). The rental yield on the “spare rooms” will be affected.

That said, this is mitigated by the fact that BTOs in the Central area can command higher rent. But who knows, perhaps rental for rooms in the Central area can be on par with rental for a whole unit in the non-mature/mature estate.

3. Smaller Pool Of Buyers

Because of the eligibility criteria, there will be a smaller pool of homebuyers that can qualify for HDBs in the Central area. Does this restrict your bargaining power as a seller in the future? Quite significantly!

The biggest limitation is the income ceiling that your potential buyers will be restricted by. Currently, the prevailing income ceiling of $14,000 means that potential buyers will be unlikely to pay more than $1 million for a resale PLH flat.

How Much Additional Subsidies Are You Getting? And How Much Will Each Unit Cost?

Because properties in the Central area are more valuable, more subsidies need to be dished out from HDB side to keep public housing affordable. Unfortunately, HDB isn’t making the additional subsidies transparent.

Instead, what it does is to price the subsidies into the indicative price range whenever the project is launched.

For River Peaks I and II, the first BTO to be classified as Central area and under the HDB PLH model, the after-subsidy price is between $582,000 and $688,000. Now, is this a fair price?

| River Peaks I and II | Kent Heights | |

|---|---|---|

| Type of Property | 4-room | 4-room |

| Est. Floor Area | 88 sqm | 92 sqm |

| Est. Internal Floor Area | 86 sqm | 90 sqm |

| Price Range | $582,000 to $688,000 | $511,000 to $660,000 |

Source: HDB

A quick comparison between the November 2021 BTO pricing between Kent Heights (Kallang) and River Peaks (Rochor) shows that they have a similar range.

Given that River Peaks is 1.5km closer to the CBD than Kent Heights, it appears that HDB has already factored in quite a sizeable subsidy into the price.

Subsidy Recovery: The Unknown In The Equation

Unlike typical HDBs, HDBs under the PLH model will be subjected to a subsidy recovery (or subsidy clawback). This will affect those who are looking to sell their HDB in the resale market. The PLH model dictates a subsidy clawback amount that needs to be repaid to HDB when you sell the property.

The rationale for this is likely because:

- You received additional subsidies from HDB at the start, so you need to pay it back (duh); and

- To discourage you from flipping your HDB and encourage only those looking for a home to stay to apply.

The subsidy recovery amount varies from project to project. It is only made known when the BTO project is launched. River Peaks at Rochor is the only BTO project launched under PLH model. For River Peaks, the subsidy recovery is 6% of the future selling price or valuation, whichever is higher.

At Mortgage Master, we know the latest home loan packages in the market and sometimes can even offer exclusive interest rate packages that you cannot get directly from the bank. If you're looking to purchase a new property, or refinance your existing home loan, fill up our enquiry form and our mortgage consultants will follow up with a call.